🔎 Amazon taking over Insurance?

Plus, Hyundai is joining the Telematics party 🎉

We’re testing a new format using Substack this month - we’d really appreciate it if you could take this one question survey to let us know what you think!

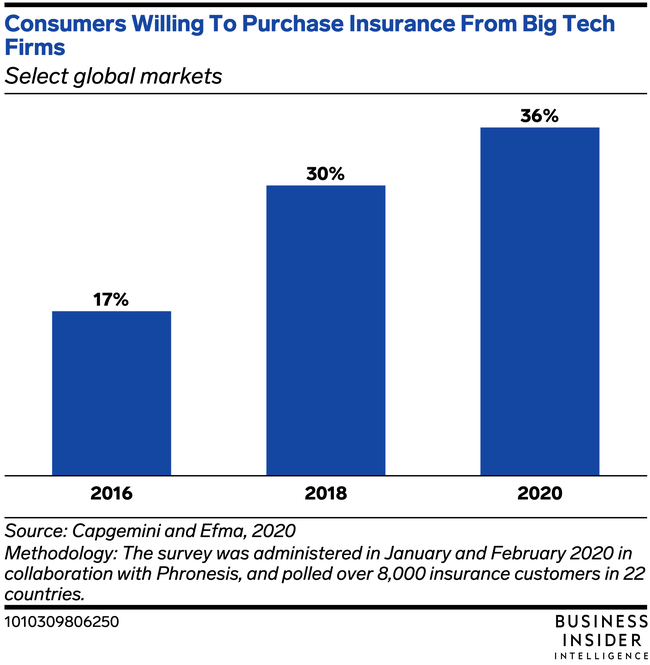

🚗 Amazon now sells auto insurance in India. The coverage will be offered via Amazon Pay and will take ~2 min with no paperwork required. The company claims that it is planning to expand its insurance service to offer coverage on health, flight, and cabs. (Read more)

Mark McLaughlin, Global Insurance Director @IBM: Insurers used to ask me all the time "when is Google going to get into insurance?" -- particularly when they were experimenting with Google Compare. My answer was "never" because it did not make financial sense for them to deal with the regulatory headaches and reserving, and that turned out to be correct. Although... (link)

Amazon, though, is a kettle of fish of another color. Amazon sells goods and increasingly, services that are insurable assets, and so there is a value proposition there that makes sense for buyers. They have been making a number of forays into the insurance space with Berkshire Hathaway, with Asurion and SquareTrade, and Travelers. They've also been expanding Amazon Pay, leveraging the same "credit card on file" access to extend reach into many new markets. Their foray into auto insurance in India is a logical step for them in this context.

Zhong An rode a similar position in China, with joint ownership by Alibaba, Tencent, and Ping An, to US$6B revenue in six years. There will be more to this Amazon insurance story. The question is, how will insurers react?

🚘 Hyundai is thinking about insurance. Hyundai is working on collecting real-time detailed vehicle data (e.g. fuel efficiency, driving habits, etc) to implement open service ecosystems like such as integrated parking reservations, driving habit-linked insurance, smart home connection solutions, and AI support. (Read more)

Eric Pilkington, Partner @IBM: This announces Hyundai’s entry into the telematics space, who’s data hose has been turned full blast in recent years. By 2025, there will be 116 million connected cars in the US — and according to one estimate by Hitachi, each of those connected cars will upload 25 gigabytes of data to the cloud per hour. If you do the math, that’s 219 terabytes each year, and by 2025, it works out to roughly 25 billion terabytes of total connected car data each year. It’s a tsunami of data that did not exist even a few years ago, and it’s about to transform the transportation and insurance industry.

The data that connected cars and autonomous vehicles produce open up entirely new revenue streams for automakers. Importantly, telematics provide auto insurance companies, logistics, fleet managers, among others, with valuable data that can be leveraged to make transportation safer and more efficient. Insurance companies can gather data from vehicles, telematics, or wireless devices and smartphones to gather data, generate driver scores, and provide feedback for safer driving. Further, auto insurers can use this data for a variety of initiatives, such as issuing behavior-based insurance and usage-based insurance policies.

Additionally, when paired with AI, mobile, and other remote sensing technologies, carriers are finding ways to transform the delivery of core services and slash resolution times and costs. Several leading P&Cs such as Metromile, Esurance, and Nationwide, and a variety of startups like Shift are using AI and other technologies to automate sales and underwriting, adjust policies dynamically by monitoring real-time driving behavior and other attributes, and analyze and process claims using AI and augmented reality.

📈 Usage-based insurance gains funding amid pandemic. Despite overall insurtech funding dropping 54% in Q1, UBI is seeing continued investment, with UBI provider By Miles recently securing £15 million in funding. The trend is projected to continue. (Read more)

Fabrice Lebegue, VP & Sr. Partner @IBM: Usage-based insurance is here to stay and grow as a market. It is a win-win for customers with potential rebates but also the promise of a substantial reduction in Claims for insurers. With the rise of IoT, telematics, data/AI, consumer behaviors (e.g lifestyle/health, driving, home security) analytics and digital connectedness allow insurers to provide their customers more and more with UBI products and create more experience stickiness.

What will be interesting is to see incumbents insurance's ability to innovate and move rapidly into this space vs. insurtech. Some incumbents are already well advanced. They are well-positioned given their customer base but they may need to acquire or partner to access a specific set of capabilities (tech, data, telematics, IoT, commercial-grade tech/data products) to keep pushing this model across their different product lines and for new disruptive ones.

✈️ Koala grabs €1.6 million to bring win-win to travel insurance. Tracking all journeys in real-time, Koala instantly informs passengers as disruption occurs and issues cash compensation on the spot, whatever the cause of the delay might be. Koala’s products benefit both operators and consumers. (Read more)

Yoann Michaux, Partner @IBM: While the approach isn't new, it is interestingly benefiting both sides: airlines and travel agencies on one end, passengers on the other vs. not just the latter. It offers yet another weapon for travel agencies and airlines to right a wrong before a customer notices it - in addition to customer feedback management systems, own workflow analysis, first and third party data and analytics, etc. Automating the last step for the customer - obtaining the compensation vs. simply informing and reminding to file a claim - seems like a no brainer next step for the company's ambition (i.e. facilitate the end-to-end travel journey at term). I'd be curious to try it once we can travel again somewhat regularly, to validate the "100%", in a travel industry prone to fine lines for conditions.

💰Hippo raises $150M for InsurTech platform. In the startup world, even a hippo can be a unicorn. Hippo disclosed that it raised $150 million in a Series E round of funding, bringing its valuation to $1.5 billion. Founded in 2015, the Palo Alto-based company focuses on policies for homeowners. (Read More)

Yoann Michaux, Partner @IBM: Interesting development for a company embodying the MVP approach to launch new products iteratively and progressively at scale, leveraging tech and data for property risk assessment as well as for constant risk re-evaluation throughout a policy tenure, creating a simple customer experience by limiting information required at onboarding or directly embedding the homeowner policy purchase as part of the mortgage process, and paired with a smart home program to detect and prevent risks within the home (leaks, security, etc).

A lot of key ingredients are leveraged here: Better customer experience, reliance on 3rd party partners to create acquisition and servicing ecosystem, synergies with the banking world through APIs, IoT, etc... And a very interesting approach to COVID and IoT adoption: offering free services and IoT devices, which would act as a key to gathering massive data to determine homeowner’s behaviors and impact on claims and overall risk, likely before expanding the approach to other IoT devices and use cases.

Contributors:

Chelsea Jeon — yerin.jeon@ibm.com

Stephanie Marino — stephanie.marino@ibm.com

Yoann Michaux — yoann.michaux@ibm.com

Mark McLaughlin — mmclau@us.ibm.com

Eric Pilkington — eric.pilkington@ibm.com

Fabrice Lebegue — fabrice.lebegue@ibm.com

Hi there! 👋 Thanks for reading IBM InsurTech Decoded. We would love your feedback. Feel free to email us at yerin.jeon@ibm.com.